Invest Path

Helping people save better

In mid-2015, the Atlantic published an article stating that 47% of Americans would struggle to resolve a $400 emergency—with some even resorting to retirement funds withdrawals. This startling fact piqued the interest of Fidelity Labs and led to the development of an incubator that would primarily focus on whether there was a real product opportunity to help people develop better savings habits. This year-long research project pushed me to expand my role as a designer and gave me an opportunity to dive deeply into the research of a complex problem rooted in human emotions, identities, and behaviors.

The Challenge

There are multiple factors that can determine a person’s financial wellness. Career choices, education, children, are just a few examples of what can alter someone’s overall financial well-being. Our team recognized the importance of the work around this statistic and got to work immediately on its analysis. The product we created had to be simple enough to not intimidate users, as a lot of financial products on the market do, and help users gain confidence that they're doing the right thing with their money.

Research

How do we approach such a broad subject?

Our research and discovery phase ran for about 6 months. We started by organizing a series of tests and experiments around the Fidelity office, and contacted internal stakeholders who were considered subject matter experts on financial wellness. Getting people to open up to us about a generally private and sensitive matter required creativity in our experimental design. So we asked people to draw what financial wellness meant to them and even physically constructed a "Financial Secrets" booth, where people anonymously jotted down their deepest, darkest financial secrets.

User interviews

We conducted 15 in-person, 90-minute interviews with individuals at different ends of the financial wellness spectrum. We looked for a mix of men, women, and couples who met certain indicators for financial strain. Our discussion was framed around three parts: an exploration of impactful financial memories, a discussion of current financial obligations, and an exploration into future financial aspirations.

Synthesis

After the interviews, we shared stories to disseminate knowledge and create a shared sense of empathy amongst our users.

What we found

Most of the people we interviewed were experiencing trouble with day-to-day cash flow. This proved to be true for both high-income and low-income households.

What we heard

To our surprise, the emotional aspects around finances greatly outweighed rational thinking.

Personas

We zeroed in on the stories of three specific households that we believed to be prime candidates for our potential product. This was followed with the development of personas that guided us throughout the design process.

Every Problem is a Potential Opportunity

How might we...

We used the identified themes and insights to highlight problem areas for our users. By reframing our insights into ‘How might we…” questions, we were able to more effectively identify potential opportunities.

How might we help people see the impact that their short-term consumption can have on their family’s future well-being?

How might we enable people to derive pride and joy from decisions that will benefit their family in the future?

How might we provide people with the support they need in order to sustain balance of their household’s present and future financial needs?

How might we reward people for creatively pursuing joy today without compromising the future?

How might we help people feel more secure with what they've accumulated for their family’s future?

How might we give people permission to treat themselves from time to time without compromising their family’s future well-being?

Design Sprints

Putting our hypothesis to the test

We coordinated a two-week design sprint with our team and other stakeholders, using our ‘How Might We…’ statements and personas to stoke ideas. Our team decided it was best to use a modified version of the Google Design Sprint method to generate concepts that we could test with users.

Design sprint outline

Monday - Deep discussions with key stakeholders about the problem we wanted to solve

Tuesday - Rapid idea generation using the “Crazy 8” method with a group voting session at the end

Wednesday - Select the top 5 ideas to expand and decide on what we wanted to build

Thursday - Design the prototype and create a testing script

Friday - Test prototypes with real users

What we tested

Insights

- People figure out what to save through trial and error—Users were delighted by our calculator, which allowed them to experiment with different amounts and timelines to the goal. It allowed them to formalize their usual mental accounting.

- Priorities are priorities until they’re not—Our users had savings goals that were important to them, but they were not immune to ”cheating” when something held an emotional or social value.

- While universally drawn to growth, many users aren’t actively searching for more return today.

- Users do not naturally associate their non-retirement savings with investing.

- Fear of the unexpected is the biggest barrier to changing a savings behavior.

Product Concept

Built for internal buy in

We were only half way there. We created product proposal in effort to share our research and get internal stakeholders excited for this new potential product offering.

The push

Users often needed a prompt when it came to thinking about what to save for. The starting screen presented a few common big-ticket items that they could choose to get started.

People need to experiment

This simple calculator helped users experiment with and personalize their goals.

Curated paths

Depending on the amount users needed to save and their personal timeline, Fidelity could offer appropriate products that would help them reach their goal.

Everyone loves a good hack

The concept of savings boosters became popular with the users we worked with because it offered different ideas to “trick” themselves into automatically and passively saving more.

Financial goal review

This screen allowed users to review their goals and gave them the opportunity to return and revise their plans as needed.

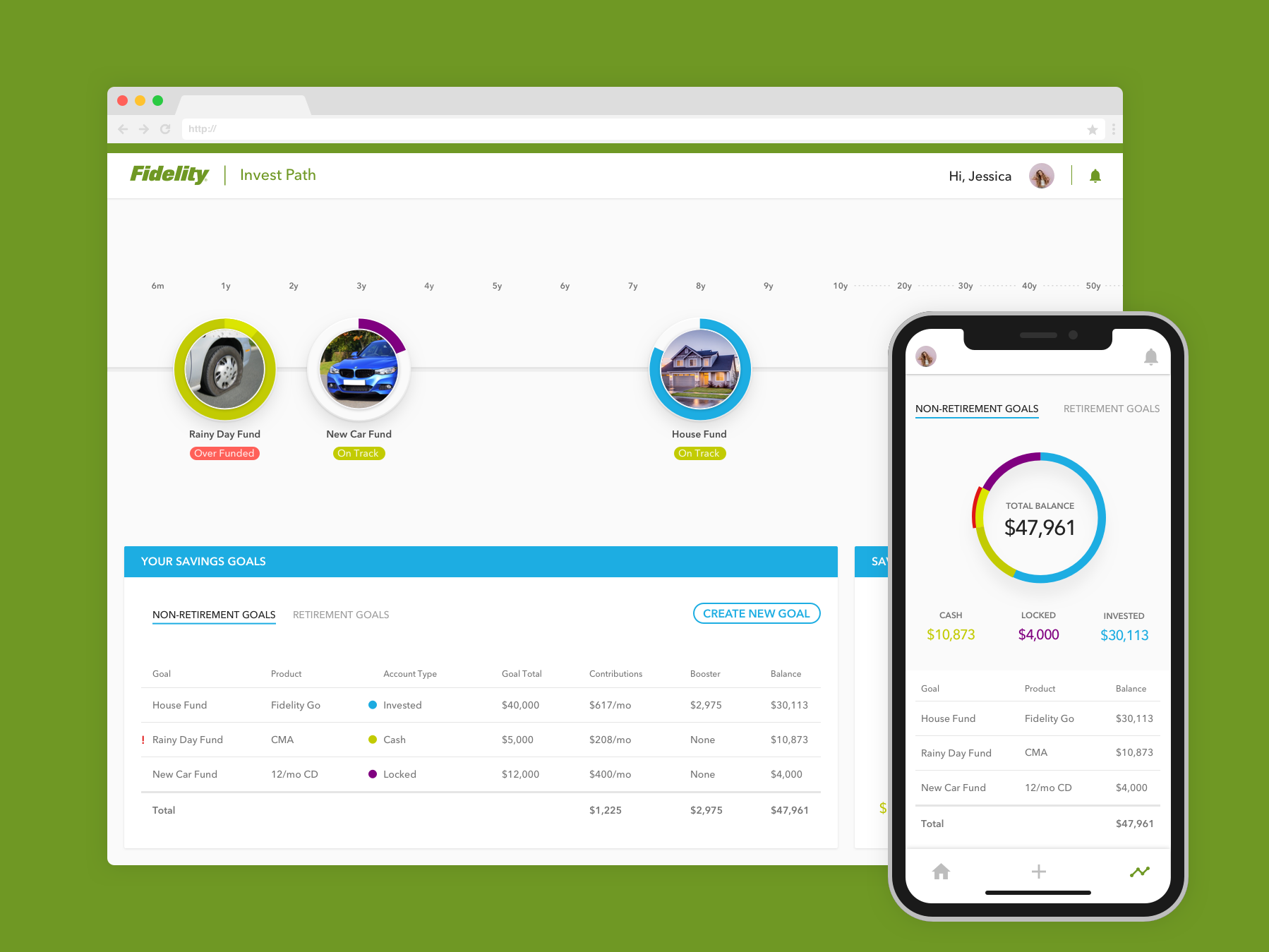

The dashboard

The dashboard gave users a simple bird's eye view of their entire financial timeline and helped them track growth along the way.

Concept for mobile

It wasn't evident if a product like this should be mobile or not, due to the behavior data our team gathered through research. Our theory was that saving is a long term exercise and should be viewed in the same manner as a retirement account. The best thing to do is to set it and forget it.

Outcome

Dead but not forgotten

Although this exact concept never materialized into a live product, our team's efforts still resonated within the company. We successfully highlighted potential customer groups that weren't currently on Fidelity's radar and helped executive leaders within the organization understand the unrealized long-term value. At the time, it was decided that developing the new application wasn't feasible, however, Fidelity still wanted to find ways to take actionable steps. The incubator was repositioned to continue the research and explore new service offerings, based on the learnings from our work.